Quick links

Registered Education Savings Plan

DCHP-2 (Feb 2013)

Spelling variants:RESP

n. �— Finance, Administration

an investment program for parents or other qualified individuals to save for their children's post-secondary education.

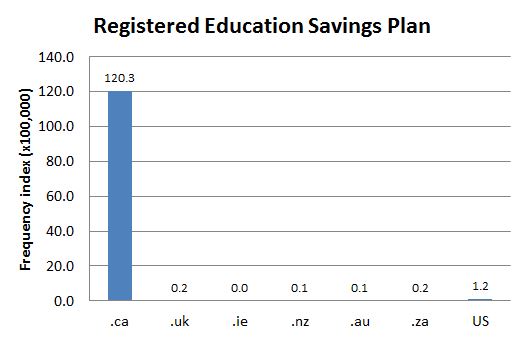

Type: 1. Origin — The Registered Education Savings Plan was introduced in 1972 (see CGA website and the 2010 quotation). It functions as a contract between a subscriber (usually a parent) and a promoter (a financial institution). The subscriber names at least one beneficiary (usually his or her child(ren)) and makes contributions on their behalf, which grow in the account tax-free until the beneficiary can withdraw the money at the age of 18 when he or she enrols in a post-secondary institution. As Chart 1 shows, the term is virtually limited to Canada.

See also COD-2, which lists the term's abbreviation (s.v. "RESP"), as "Cdn".

See also COD-2, which lists the term's abbreviation (s.v. "RESP"), as "Cdn".

See: RESP

As with other Canada-backed financial products, such as RRSP or GIC, the letter abbreviation is the more commonly used form.

Quotations

1978

A RESP is of special benefit to a student who pursues his or her education right through university, but less so for a drop-out. Contributions for the latter can be returned - but without the accumulated interest.

1985

You may be able to effectively defer and possibly eventually avoid the payment of tax on investment income, within certain limitations, by making contributions to a registered educational savings plan (RESP) for the university education of your children or grandchildren.

1987

The provincial government said it will look at the possibility of offering a tax-deductible "registered educational savings plan," will give "credits" to top secondary school students towards the cost of post-secondary education and will match corporate and private donations towards scholarships.

1989

Ask for registered education savings plan literature; an RESP also allows tax-free growth, with this growth belonging to the student for tax purposes.

1995

If you're reasonably sure your kids will attend a post-secondary institution, you might want to contribute to an RESP, a registered education savings plan.

2005

For every dollar contributed to a Registered Education Savings Plan, the federal government said it would contribute 20 cents, up to $400 each year.

2010

The RESP was first introduced in 1972 by the federal government to provide Canadian families with an inducement to save for higher education. An RESP allows for continuous contributions to be made to a registered savings account where earnings accumulate tax free.

The RESP has simply become a sensible opportunity for families to support the future of their children's educations. To encourage savings through RESPs, the government has provided incentives by contributing funds to savings plans based on participant contributions. With these enhancements, the structure of the RESP has transformed itself from a generic savings account to a more advantageous savings vehicle.

2013

RESPs are an effective and popular way to save for your child's future education and help families get further money from the Government of Canada. Once you open an RESP, the money you contribute, plus any money your child receives from the Government of Canada, starts to grow. At the same time, you are encouraging your child to continue his or her education after high school.

References

- CGA Canada

- COD-2

Images